2026 세계경제통상전망 세미나에서도 AI 인프라 투자와 반도체 공급망 이슈가 핵심 키워드로 강조되었습니다. 특히 AI 서버 중심의 데이터센터 확장은 반도체·메모리 수요를 넘어 장비와 제조 영역까지 영향을 미치고 있습니다.

그렇다면 AI 반도체의 성장은 장비 산업에 어떤 변화를 가져올까요?

As AI technology advances, rising memory demand and semiconductor supply chain issues are reshaping the industrial landscape.

At the 2026 Global Economic and Trade Outlook Seminar, AI infrastructure investment and long-term industrial transformation were key themes. As AI data centers expand, their impact is rapidly extending into equipment and manufacturing.

How will the growth of AI semiconductors reshape the equipment industry?

AI 반도체 산업의 성장을 짚어보기 전에,

2026년 세계경제와 환율·무역 환경의 큰 흐름을 Ep.2에서 먼저 확인해 보세요 !

Before diving into the growth of the AI semiconductor industry,

take a look at Ep.2 for a broader view of the 2026 global economy, FX, and trade environment !

OpenAI의 AI 인프라 확장 전략

OpenAI’s AI Infrastructure Expansion Strategy

AI 반도체 수요 확대의 출발점에는 AI 인프라에 대한 공격적인 투자가 있습니다. 특히 OpenAI의 인프라 확장 계획은 AI 기술 발전이 얼마나 빠르게 물리적 인프라 수요로 전환되고 있는지를 보여줍니다. 현재 가동 중인 AI 인프라 규모는 약 2GW 수준이지만, 이는 본격적인 확장의 시작에 불과합니다.

시장에서는 2025년 하반기(2H25)를 전후해 OpenAI가 약 38.2GW 규모의 신규 AI 인프라를 확보할 것으로 보고 있습니다. 더 나아가 OpenAI는 장기적으로 250GW 규모의 AI 인프라 구축을 목표로 하고 있는 것으로 알려졌습니다. 기존과 신규 인프라를 모두 합해도 약 40.2GW로, 장기 목표 대비 달성률은 15% 수준에 그칩니다. 이는 AI 인프라 투자가 아직 초기 단계에 있으며, 향후에도 데이터센터·AI 서버·반도체·장비·제조 영역 전반에 걸친 지속적인 수요 확대가 이어질 가능성이 높다는 점을 시사합니다.

The expansion of AI semiconductor demand is being driven by aggressive investment in AI infrastructure. In this context, OpenAI’s infrastructure roadmap clearly illustrates how rapidly advances in AI technology are translating into demand for physical infrastructure. At present, OpenAI is operating approximately 2GW of AI infrastructure—an important milestone, but only the starting point of a much larger expansion.

Market estimates suggest that by 2H25, OpenAI will have secured around 38.2GW of new AI infrastructure capacity. Beyond this mid-term expansion, OpenAI is also understood to be targeting a long-term goal of 250GW in total AI infrastructure. Even when combining existing capacity (2GW) with the expected new additions (38.2GW), total capacity would reach only 40.2GW, representing roughly 15% of the long-term target. This gap indicates that AI infrastructure investment is still in an early phase and suggests that sustained demand growth is likely to continue across data centers, AI servers, semiconductors, equipment, and manufacturing in the years ahead.

AI 시장의 폭발적 성장과 인프라 중심 구조 전환

Explosive Growth of the AI Market and the Shift Toward an Infrastructure-Centric Model

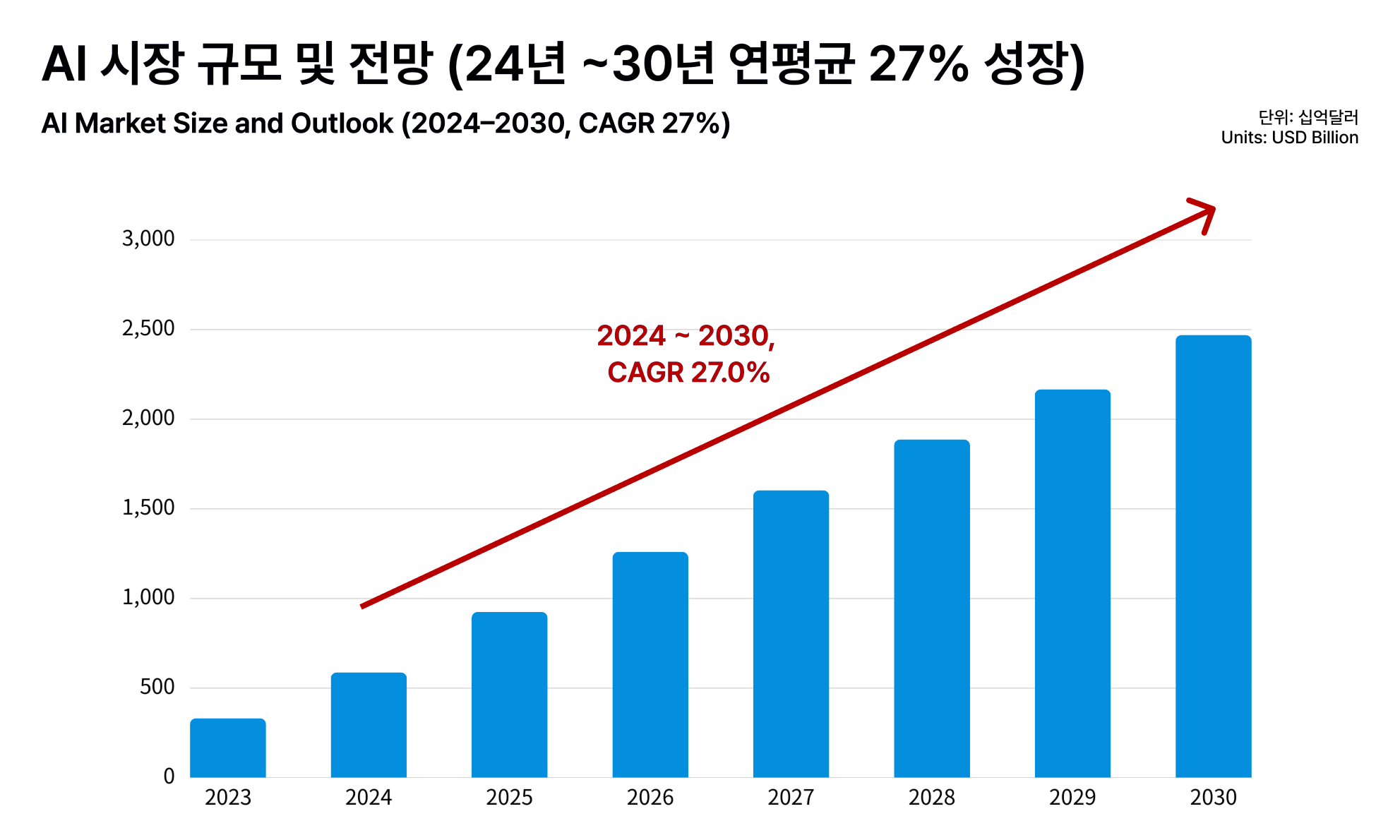

AI 시장은 단기 유행이 아닌 중장기 산업 성장을 이끄는 핵심 축으로 빠르게 확대되고 있습니다. 전망에 따르면 AI 시장 규모는 2030년 2.47조 달러에 이를 것으로 예상되며, 2024~2030년 연평균 성장률(CAGR)은 27%에 달합니다. PC와 스마트폰 등 디바이스 영역까지 포함할 경우, 2030년 AI 시장은 최대 3.2조 달러까지 확대될 가능성도 제시되고 있습니다. 실제로 글로벌 AI 컨퍼런스에서는 2030년 AI 시장이 3~4조 달러 규모로 성장할 것이라는 전망도 공유된 바 있습니다.

특히 주목할 점은 AI 시장 성장의 무게 중심이 소프트웨어를 넘어 인프라로 이동하고 있다는 점입니다. 2030년까지 AI 인프라 시장(인프라 SW 포함)은 약 1.19조 달러 규모로 성장해 전체 AI 시장의 48%를 차지할 것으로 예상되며, 연평균 성장률은 31%로 소프트웨어보다 더 빠른 성장세를 보일 전망입니다. 데이터센터는 AI 서버 중심으로 재편되고 있으며, AI 서버는 기존 서버 대비 전력·연산·메모리 소모가 월등히 높은 구조를 갖고 있습니다. 이로 인해 AI 시장의 성장은 자연스럽게 반도체·메모리·전력·장비·제조 영역 전반에 구조적인 수요 확대를 만들어내고 있습니다.

The AI market is rapidly expanding as a core driver of mid- to long-term industrial growth, rather than a short-lived trend. According to market forecasts, the global AI market is expected to reach USD 2.47 trillion by 2030, with a CAGR of 27% from 2024 to 2030. When device segments such as PCs and smartphones are included, the AI market could grow to as much as USD 3.2 trillion by 2030. Discussions at global AI conferences have also pointed to projections of an AI market reaching USD 3 to 4 trillion by the end of the decade.

What stands out most is that the center of gravity in AI growth is shifting beyond software toward infrastructure. By 2030, the AI infrastructure market, including infrastructure software, is expected to reach approximately USD 1.19 trillion, accounting for 48% of the total AI market, with a projected CAGR of 31%, outpacing software growth. Data centers are increasingly being restructured around AI servers, which require significantly higher levels of power, computing capacity, and memory than conventional servers. As a result, the expansion of the AI market is naturally translating into structural demand growth across semiconductors, memory, power systems, equipment, and manufacturing.

메모리 수요 증가와 Memory Wall 이슈

Growing Memory Demand and the Memory Wall Challenge

AI 기술이 발전할수록 메모리 요구량은 오히려 더 빠르게 증가하고 있습니다. 연산 성능은 GPU와 ASIC을 중심으로 빠르게 확장되고 있지만, 메모리 기술의 발전 속도는 이에 미치지 못하고 있기 때문입니다. 대규모 언어모델(LLM)의 확산과 함께 토큰(Token) 처리량이 급격히 증가하면서, AI 컴퓨팅의 성능은 연산 능력이 아니라 메모리 용량과 대역폭에 의해 제한되는 단계에 접어들고 있습니다. 특히 학습에서 추론으로 AI 활용이 이동하면서 하드웨어 부담이 줄어들 것이라는 초기 예상과 달리, 추론 단계가 오히려 더 많은 메모리 자원을 요구하는 구조가 확인되고 있습니다. 이로 인해 AI 컴퓨팅 전반에서 Memory Wall, 즉 연산 성능과 메모리 성능 간 격차 문제가 본격적으로 부각되고 있습니다.

As AI technology advances, memory requirements are increasing at an even faster pace. While computing performance continues to scale rapidly, driven by GPUs and ASICs, the pace of progress in memory technology has not kept up. With the widespread adoption of large language models (LLMs), the volume of token processing has surged, pushing AI computing into a phase where performance is constrained less by raw compute and more by memory capacity and bandwidth. Contrary to early assumptions that hardware demands would ease as AI workloads shifted from training to inference, it has become clear that inference workloads often require even greater memory resources. As a result, the Memory Wall, defined as the widening gap between compute performance and memory performance, is emerging as a critical bottleneck across AI computing.

이러한 메모리 병목 현상은 특정 기업이나 아키텍처의 문제가 아니라, AI 컴퓨팅 구조 자체의 한계를 의미합니다. 엔비디아 GPU뿐 아니라 구글 TPU와 같은 ASIC 역시 메모리 사용량과 대역폭을 빠르게 확대하며 GPU와 유사한 수준으로 접근하고 있습니다. 이는 무어의 법칙이 사실상 종료된 메모리 영역에서, 단순한 설계 혁신만으로는 AI 성능 향상을 이어가기 어렵다는 점을 보여줍니다. 결국 AI 성능 경쟁의 핵심은 메모리를 어떻게 구현하고, 얼마나 정밀하게 집적·연결할 수 있는가로 이동하고 있으며, 이는 곧 고급 공정 기술, 패키징, 정밀 가공, 그리고 이를 가능하게 하는 제조·장비 역량의 중요성을 다시 부각시키고 있습니다.

This memory bottleneck is not a challenge tied to any single company or architecture; it reflects structural limits within AI computing itself. In addition to NVIDIA GPUs, ASICs such as Google’s TPUs are rapidly increasing memory capacity and bandwidth, approaching levels comparable to GPUs. This trend underscores the reality that in the memory domain, where Moore’s Law has effectively run its course, design innovation alone is no longer sufficient to sustain AI performance gains. Consequently, the focus of AI performance competition is shifting toward how memory is implemented, how densely it can be integrated, and how precisely it can be interconnected, elevating the importance of advanced process technologies, packaging, precision machining, and the manufacturing and equipment capabilities that enable them.

글로벌 반도체 공급망의 현실

The Reality of the Global Semiconductor Supply Chain

AI 반도체 수요가 구조적으로 확대되는 가운데, 이를 실제로 생산·공급할 수 있는 글로벌 반도체 공급망의 현실은 여전히 제한적입니다. 특히 최선단 공정 영역에서는 TSMC의 역할이 절대적입니다. TSMC는 미국·일본·독일 등으로 생산 거점을 확대하고 있지만, 전체 생산 능력의 약 90%는 여전히 대만에 집중되어 있으며, 최선단 공정의 양산 라인과 R&D 역량은 사실상 100% 대만에 위치해 있습니다. 이는 단순한 비용 문제가 아니라, 수십 년에 걸쳐 구축된 초고밀도 반도체 생태계와 공급망 집적 효과가 단기간에 다른 지역으로 이전되기 어렵기 때문입니다.

As demand for AI semiconductors continues to expand structurally, the reality of the global semiconductor supply chain capable of producing and delivering them remains constrained. In particular, TSMC plays an indispensable role in the most advanced process nodes. While TSMC is expanding production footprints into the United States, Japan, and Germany, approximately 90% of its total manufacturing capacity remains concentrated in Taiwan. Moreover, nearly 100% of its leading edge mass production lines and R&D capabilities are still located there. This concentration is not simply a matter of cost. It reflects the fact that a highly dense semiconductor ecosystem and accumulated supply chain integration, built over decades, cannot be relocated to other regions in a short period of time.

이러한 구조는 각국의 반도체 자급화 전략이 현실적으로 한계를 가질 수밖에 없음을 보여줍니다. 반도체는 어느 한 국가가 100% 자급할 수 없는 산업이며, 실제로 글로벌 공급망은 국가별 강점에 따라 더욱 분업화되고 있습니다. 미국은 설계·AI 반도체 수요, 대만은 파운드리와 첨단 패키징, 한국과 일본은 메모리와 핵심 제조 장비, 중국은 중저가 공정과 내수 기반 확대에 집중하는 구조입니다. 관세나 보호무역 정책은 비용을 높일 수는 있지만, AI 반도체와 같은 고급 기술 수요를 근본적으로 억제하기는 어렵습니다. 결국 글로벌 반도체 공급망은 지정학적 긴장 속에서도 유지·재편될 가능성이 높으며, 이는 장기적으로 제조 공정과 장비 경쟁력을 보유한 국가와 기업의 전략적 가치가 더욱 커질 것임을 시사합니다.

This structure highlights the practical limits of national semiconductor self sufficiency strategies. Semiconductors are not an industry that any single country can fully localize on its own, and global supply chains are becoming increasingly specialized based on regional strengths. The United States focuses on chip design and AI semiconductor demand, Taiwan on foundry services and advanced packaging, Korea and Japan on memory and critical manufacturing equipment, and China on mature process nodes and domestic market expansion. While tariffs and protectionist policies may increase costs, they are unlikely to fundamentally suppress demand for advanced technologies such as AI semiconductors. Ultimately, the global semiconductor supply chain is likely to persist and be reshaped even amid geopolitical tensions, reinforcing the long term strategic value of countries and companies with strong manufacturing process and equipment capabilities.

AI 반도체 시장이 주는 산업적 시사점

Industrial Implications of the AI Semiconductor Market

AI 반도체 시장의 성장은 단기적인 기술 트렌드가 아니라, 중장기적으로 지속될 구조적 수요라는 점에서 산업적 의미가 큽니다. 앞서 살펴본 것처럼 AI 인프라 확대, 메모리 병목(Memory Wall), 그리고 글로벌 공급망의 고착화는 모두 관세나 정책 변화만으로는 수요를 억제하기 어려운 구조를 형성하고 있습니다. 실제로 반도체 산업에서 관세의 영향은 제한적인 반면, AI 서버·메모리·첨단 공정에 대한 투자는 중단 없이 이어지고 있습니다. 이는 AI 반도체 수요가 경기나 정책보다 기술 구조와 산업 필연성에 의해 움직이고 있음을 의미합니다.

The growth of the AI semiconductor market carries significant industrial implications, as it represents structural demand that is likely to persist over the mid to long term, rather than a short term technology trend. As discussed earlier, the expansion of AI infrastructure, the emergence of the Memory Wall, and the consolidation of the global supply chain all form a structure in which demand is difficult to suppress through tariffs or policy changes alone. In practice, while the impact of tariffs on the semiconductor industry remains limited, investment in AI servers, memory, and advanced manufacturing processes continues without interruption. This indicates that AI semiconductor demand is being driven less by economic cycles or policy decisions and more by technological structure and industrial necessity.

이러한 환경에서 산업 경쟁력의 핵심은 점차 설계 중심에서 제조·공정·장비 역량 중심으로 이동하고 있습니다. AI 성능을 좌우하는 메모리 구현, 패키징, 미세 공정 안정성은 모두 정밀한 설비와 고도화된 제조 기술 없이는 달성하기 어렵기 때문입니다. 이는 공작기계·정밀가공·제조 장비 산업에 있어 명확한 기회 요인으로 작용합니다. 변동성이 큰 글로벌 환경 속에서도, 기술·설비·제조 역량을 갖춘 기업은 AI 반도체 산업 성장의 흐름 속에서 지속 가능한 파트너이자 핵심 인프라 공급자로 자리매김할 가능성이 높아지고 있습니다.

Within this environment, the core of industrial competitiveness is gradually shifting away from design centric advantages toward manufacturing, process, and equipment capabilities. Key factors that determine AI performance, such as memory implementation, advanced packaging, and the stability of leading edge processes, cannot be achieved without high precision equipment and sophisticated manufacturing technologies. This shift presents a clear opportunity for industries related to machine tools, precision machining, and manufacturing equipment. Even amid heightened global uncertainty, companies with strong capabilities in technology, equipment, and manufacturing are increasingly well positioned to establish themselves as sustainable partners and critical infrastructure providers within the ongoing growth of the AI semiconductor industry.

고도화된 반도체 제조 공정을 위한 오알에스코리아의 정밀 설비 기술

Precision Equipment Technologies from ORSKOREA for Advanced Semiconductor Manufacturing Processes

이러한 변화는 실제 반도체 제조 공정에서도 구체적인 요구로 나타나고 있습니다. 고집적 메모리와 첨단 패키징 환경에서는 공정 안정성과 정밀 제어 능력이 수율을 좌우하는 핵심 요소로 작용하며, 스핀들의 회전 특성과 연삭 공정의 제어 방식 역시 중요한 변수로 떠오르고 있습니다.

반도체 제조 현장에서 오알에스코리아의 유정압 스핀들과 수직양두연삭기가 어떤 역할을 하는지에 대해서는, 아래의 관련 아티클을 통해 보다 구체적으로 살펴볼 수 있습니다.

These shifts are translating into clear and tangible requirements within semiconductor manufacturing environments. In highly integrated memory and advanced packaging processes, process stability and precise controllability have become critical factors directly influencing yield. In this context, spindle rotational characteristics and the control methodology of grinding processes are emerging as key variables in achieving consistent and reliable manufacturing outcomes.

For a closer look at how ORSKOREA’s hydrostatic spindles and vertical double disc grinding machines are applied in real semiconductor manufacturing settings, further details can be found in the related articles below, which explore their roles and technical considerations in greater depth.

이번 세계경제통상세미나에 참석한 오알에스코리아 영업팀 강승헌 사원과 세빈치 달그치 사원은, 올해 수출 동향과 향후 관세 흐름에 대한 실질적인 인사이트를 확인할 수 있었다고 전했습니다. 특히 데이터센터를 중심으로 한 AI 인프라 투자가 지속되면서, 반도체 산업의 중장기 성장 가능성이 여전히 유효하다는 점이 인상 깊었다는 의견이었습니다.

또한 미국의 정치·통상 환경 변화에 따라 북미와 남미 시장에서는 현지 생산과 네트워크 확보의 중요성이 더욱 커지고 있는 만큼, 반도체 산업을 둘러싼 경쟁력 역시 설계나 기술을 넘어 제조 역량과 현지 대응 전략으로 확장되고 있음을 다시 한 번 확인하는 자리였습니다. 오알에스코리아는 AI 반도체를 둘러싼 이러한 구조적 변화 속에서, 앞으로 어떤 준비와 선택이 필요한지에 대한 고민은 계속 이어질 것입니다.

At the recent Global Economic and Trade Outlook Seminar, ORSKOREA sales team members Kang Seungheon and Sevinc Dalgic shared that the event provided practical insights into current export trends and the evolving outlook for tariffs. They noted that continued investment in AI infrastructure, particularly data center driven expansion, reinforces the view that the mid to long term growth potential of the semiconductor industry remains firmly intact.

They also highlighted that changes in the US political and trade environment are increasing the importance of local production and on site networks across North and South American markets. As a result, competitiveness in the semiconductor industry is increasingly extending beyond design and technology into manufacturing capability and localized response strategies. Within these structural changes surrounding AI semiconductors, ORSKOREA will continue to consider what preparations and strategic choices are required moving forward.