이번 글에서는 “2025년 수출 성적표는 2026년 전략의 출발점”이라는 문제의식을 바탕으로, 2025년 한국 수출입 동향이 어떠한 흐름을 보였는지를 중심으로 살펴봅니다.

Export trends have always been one of the earliest indicators of a country’s economic direction. Despite the global economic slowdown and ongoing geopolitical uncertainty, Korea’s trade performance in 2025 showed a steady yet meaningful recovery, leaving important implications for the broader economy.

Based on the premise that “the 2025 export performance serves as the starting point for strategies in 2026,” this article focuses on how Korea’s exports and imports evolved in 2025, examining the key trends and patterns observed during the year.

2026 세계경제통상전망 세미나

2026 Global Economic and Trade Outlook Seminar

오알에스코리아는 2026년 경제 흐름과 무역 환경 변화를 보다 정확히 이해하기 위해 세계 경제 통상 세미나에 참석했습니다. 이번 세미나에서는 2025년 한국 수출입 성과를 점검하고, 이를 토대로 2026년 세계 경제와 무역 환경을 어떻게 해석해야 할지에 대한 다양한 시각이 공유되었습니다. 이러한 논의를 바탕으로, 수출·경제·환율 흐름에 따른 주요 인사이트를 함께 공유하고자 합니다.

ORSKOREA attended the Global Economic and Trade Outlook Seminar to gain a more accurate understanding of economic trends and changes in the trade environment heading into 2026.

During the seminar, participants reviewed Korea’s export and import performance in 2025 and shared diverse perspectives on how to interpret the global economic and trade environment for 2026. Based on these discussions, ORSKOREA aims to share key insights derived from export, economic, and exchange rate trends.

2025년 한국 수출입 동향 한눈에 보기

2025 Korea’s Export & Import Trends at a Glance

2025년 1~10월 기준, 한국 수출은 5,792억 달러로 전년 동기 대비 2.3% 증가했습니다. 같은 기간 수입은 5,228억 달러로 0.6% 감소했으며, 이에 따라 무역수지는 564억 달러 흑자를 기록했습니다. 수출 회복과 수입 조정이 동시에 나타나면서, 전반적인 무역 흐름은 비교적 안정적인 구조를 유지했습니다.

이번 수출 성과는 급격한 반등보다는 완만한 회복 흐름에 가깝습니다. 글로벌 경제 둔화와 지정학적 불확실성, 변동성이 이어진 환율 환경 속에서도 수출 증가세가 유지되었다는 점에서 의미가 있습니다. 특히 수출 확대와 함께 무역수지 흑자가 이어졌다는 점은, 2025년 한국 경제가 대외 환경 변화에 일정 수준 대응력을 갖추고 있음을 시사합니다.

From January to October 2025, Korea’s exports totaled USD 579.2 billion, representing a 2.3% increase year on year. During the same period, imports declined by 0.6% to USD 522.8 billion, resulting in a trade surplus of USD 56.4 billion. As export recovery and import adjustments occurred simultaneously, overall trade conditions remained relatively stable.

This export performance reflects a gradual recovery rather than a sharp rebound. The fact that export growth was sustained despite a global economic slowdown, geopolitical uncertainty, and a volatile exchange rate environment is particularly noteworthy. Moreover, the continued trade surplus alongside expanding exports suggests that Korea’s economy maintained a certain degree of resilience in responding to external economic challenges in 2025.

주요 시장 수출 변화와 제3시장 전환의 의미

Export Shifts in Major Markets and the Move Toward Third Markets

2025년 한국 수출은 주요 시장별로 상반된 흐름을 보였습니다. 중국 수출은 –3.8% 감소했으며, 미중 통상 갈등과 중국 내 수요 둔화 등의 영향이 반영된 것으로 해석됩니다. 미국 수출 역시 –5.0% 감소하며 부진한 모습을 보였으며, 전방위적 관세 부과 정책의 영향으로 특히 상호관세 15%가 시행된 직후인 8월에는 수출이 12.1% 급감했습니다. 2025년 대미 수출은 2016년 이후 9년 만에 처음으로 마이너스 증가율을 기록했으며, 자동차·자동차 부품·철강 등 고율 관세가 적용된 품목을 중심으로 감소 폭이 컸습니다. 다만 해당 품목을 제외할 경우 대미 수출은 증가한 것으로 나타나, 관세 영향이 특정 산업에 집중되어 있음을 보여줍니다.

In 2025, Korea’s exports showed contrasting trends across major markets. Exports to China fell by 3.8%, reflecting the impact of U.S. China trade tensions and weaker domestic demand in China.

Exports to the United States declined by 5.0%, remaining under pressure amid broad tariff measures. In particular, exports dropped sharply by 12.1% in August, immediately after the introduction of a 15% reciprocal tariff. As a result, exports to the U.S. recorded their first negative growth rate since 2016, with the steepest declines concentrated in automobiles, auto parts, and steel, which were subject to high tariffs. Excluding these items, however, exports to the U.S. actually increased, indicating that the tariff impact was concentrated in specific industries rather than across the broader export base.

반면 EU(+3.9%)와 아세안(+5.5%) 수출은 증가하며 전체 수출 흐름을 보완했습니다. 자동차, 선박, 방산, 반도체 등 주력 품목을 중심으로 수출이 확대됐고, 특히 대만 수출은 51.0% 증가하며 AI용 반도체와 반도체 장비 수요 확대가 직접적인 성장 요인으로 작용했습니다. 이러한 흐름은 환율 효과보다는 글로벌 산업 구조와 수요 변화에 대응한 결과로 해석됩니다.

결과적으로 2025년에는 EU·아세안·대만 등 제3시장으로의 수출 전환이 진행되며, 대미·대중 수출 부진의 영향을 완화했습니다. 이는 한국 경제와 수출 구조가 단일 시장 의존에서 벗어나 리스크 분산형으로 이동하고 있음을 보여주는 핵심 신호라고 볼 수 있습니다.

By contrast, exports to the EU rose by 3.9% and exports to ASEAN increased by 5.5%, helping to support overall export performance. Growth was led by key industries such as automobiles, ships, defense equipment, and semiconductors. In particular, exports to Taiwan surged by 51.0%, driven directly by rising demand for AI related semiconductors and semiconductor manufacturing equipment.

These trends are better explained by shifts in global industrial structure and demand, rather than by exchange rate effects. As a result, in 2025, export diversification toward third markets such as the EU, ASEAN, and Taiwan helped offset weaker exports to the United States and China. This shift represents a key signal that Korea’s economy and export structure are moving away from single market dependence toward a more risk diversified model.

수입 동향으로 본 산업 구조 변화

Industrial Structural Changes Reflected in Import Trends

2025년 1~10월 기준, 한국 수입은 5,228억 달러로 전년 대비 0.6% 감소하며 전반적으로 안정적인 흐름을 보였습니다. 다만 전체 수입 감소와 달리, 반도체와 IT 관련 품목 수입은 증가하며 산업 구조 측면에서 의미 있는 변화가 나타났습니다. 반도체 수입은 5.3% 증가했고, 컴퓨터 등 IT 품목 수입도 16.5% 확대되면서, 글로벌 경제 환경과 환율 변동성 속에서도 핵심 산업에 대한 투자가 지속되고 있음을 보여줍니다.

From January to October 2025, Korea’s imports totaled USD 522.8 billion, declining by 0.6% year on year, reflecting an overall stable trend. However, despite the decrease in total imports, imports of semiconductors and IT-related products increased, indicating meaningful structural shifts within the industrial landscape. Semiconductor imports rose by 5.3%, while imports of IT products such as computers expanded by 16.5%, demonstrating that investment in core industries continued even amid a challenging global economic environment and heightened exchange rate volatility.

특히 전기차(+63.5%)·하이브리드차(+10.9%) 관련 수입이 증가하면서 전기차 생산에 필요한 부품·소재 수입도 함께 급증했습니다. 이런 수입 구조는 단순 소비 확대가 아니라, 국내 제조업이 친환경차 전환과 생산 확대에 맞춰 공급망을 재구성하고 있다는 신호로 볼 수 있습니다.

동시에 핵심 부품·소재의 해외 의존이 커질수록 환율 변동이 원가와 수익성에 미치는 영향도 커지기 때문에, 2026년에는 구매·조달 전략과 환율 대응을 함께 설계하는 접근이 필요합니다.

In particular, imports related to electric vehicles increased by 63.5% and imports linked to hybrid vehicles rose by 10.9%, alongside a sharp increase in imports of components and materials required for electric vehicle production. This import pattern reflects more than an expansion in consumer demand. It signals that domestic manufacturers are restructuring supply chains in line with the transition to eco friendly vehicles and the expansion of production capacity.

At the same time, as dependence on overseas sources for key components and materials increases, exchange rate fluctuations have a greater impact on costs and profitability. As a result, in 2026, companies will need to adopt an integrated approach that aligns purchasing and sourcing strategies with exchange rate management.

2025년 수출을 이끈 핵심 품목

Key Products Driving Exports in 2025

2025년 한국 수출은 일부 주력 품목을 중심으로 회복 흐름을 이어갔습니다. 전반적인 경제 여건이 불확실한 상황에서도, 산업별로는 뚜렷한 온도 차가 나타났으며 이는 향후 수출 전략과 환율 환경을 해석하는 데 중요한 단서가 됩니다

In 2025, Korea’s exports continued a recovery trend driven by several key industries. Despite ongoing uncertainty in overall economic conditions, clear differences emerged across industries, offering important clues for interpreting future export strategies and the evolving exchange rate environment.

반도체: AI·장비 중심 성장

Semiconductors: Growth Driven by AI and Manufacturing Equipment

반도체 수출은 전년 대비 17.8% 증가하며 2025년 한국 수출을 이끈 핵심 품목으로 자리했습니다. 특히 AI용 반도체와 반도체 장비를 중심으로 수요가 확대되면서, 글로벌 경제 환경 속에서도 비교적 안정적인 성장세를 유지했습니다.

AI 투자 확대와 데이터센터 수요 증가는 단기적인 유행보다는 구조적인 흐름으로 평가되며, 이는 환율 변동성에도 불구하고 반도체 수출이 견조하게 유지된 배경으로 작용했습니다.

Semiconductor exports increased by 17.8% year on year, establishing semiconductors as a key product driving Korea’s exports in 2025. Demand expanded primarily for AI related semiconductors and semiconductor manufacturing equipment, allowing the sector to maintain relatively stable growth even amid a challenging global economic environment.

The expansion of AI investment and rising demand for data centers are viewed not as short term trends but as structural developments. These factors supported resilient semiconductor exports despite heightened exchange rate volatility.

자동차: 지역별 온도차와 관세 영향

Automobiles: Regional Divergence and Tariff Impact

자동차 수출은 0.9% 증가하며 완만한 흐름을 보였습니다. 다만 북미 지역으로의 수출은 관세 영향과 현지 생산 확대 흐름으로 다소 부진한 반면, EU·중남미·중동을 중심으로 친환경차 수출이 증가하며 전체 수출을 방어했습니다.

자동차 부품 수출의 증가율은 둔화되었으며, 이는 환율 요인과 더불어 통상 환경 변화가 복합적으로 작용한 결과로 해석됩니다. 자동차 산업 역시 수출 구조와 시장 전략을 함께 고려해야 하는 국면에 진입한 것으로 보입니다.

Automobile exports increased by 0.9%, showing a moderate growth trend in 2025. However, exports to North America remained relatively weak due to the impact of tariffs and the expansion of local production. In contrast, exports of eco friendly vehicles increased in markets such as the EU, Latin America, and the Middle East, helping to support overall export performance.

Growth in exports of automobile parts slowed, reflecting the combined effects of exchange rate factors and changes in the global trade environment. As a result, the automotive industry has entered a phase in which export structure and market strategy must be considered together when planning future growth.

선박: 과거 수주 물량의 본격 반영

Ship: Delivery of Previously Secured Orders

선박 수출은 전년 대비 34.5% 증가하며 가장 높은 성장률을 기록했습니다. 이는 2022~2023년에 수주된 물량이 2025년에 본격적으로 인도되면서 나타난 결과입니다.

선박 수출 증가는 단기적인 경제 변수보다는 산업 사이클의 영향이 크며, 환율 변동과 관계없이 중장기 경쟁력이 수출 실적으로 이어진 사례로 볼 수 있습니다.

Ship exports recorded the highest growth rate, increasing by 34.5% year on year. This growth reflects the delivery of vessels ordered during the 2022 to 2023 period, which began to be recognized in export figures in 2025.

The increase in ship exports was driven more by industry cycle dynamics than by short term economic variables, demonstrating how long term competitiveness can translate into export performance regardless of exchange rate fluctuations.

이처럼 2025년 수출을 이끈 핵심 품목들은 각기 다른 배경과 요인 속에서 성장했습니다. 이는 한국 경제와 수출 구조가 단일 산업에 의존하기보다는, 산업별 역할이 분화되는 단계에 접어들었음을 시사합니다.

Taken together, the key products that led exports in 2025 grew under different conditions and drivers. This indicates that Korea’s economy and export structure are moving toward a more diversified model, with distinct roles emerging across industries rather than reliance on a single sector.

신산업 수출 확대가 의미하는 구조적 변화

Structural Changes Signaled by the Expansion of Emerging Industry Exports

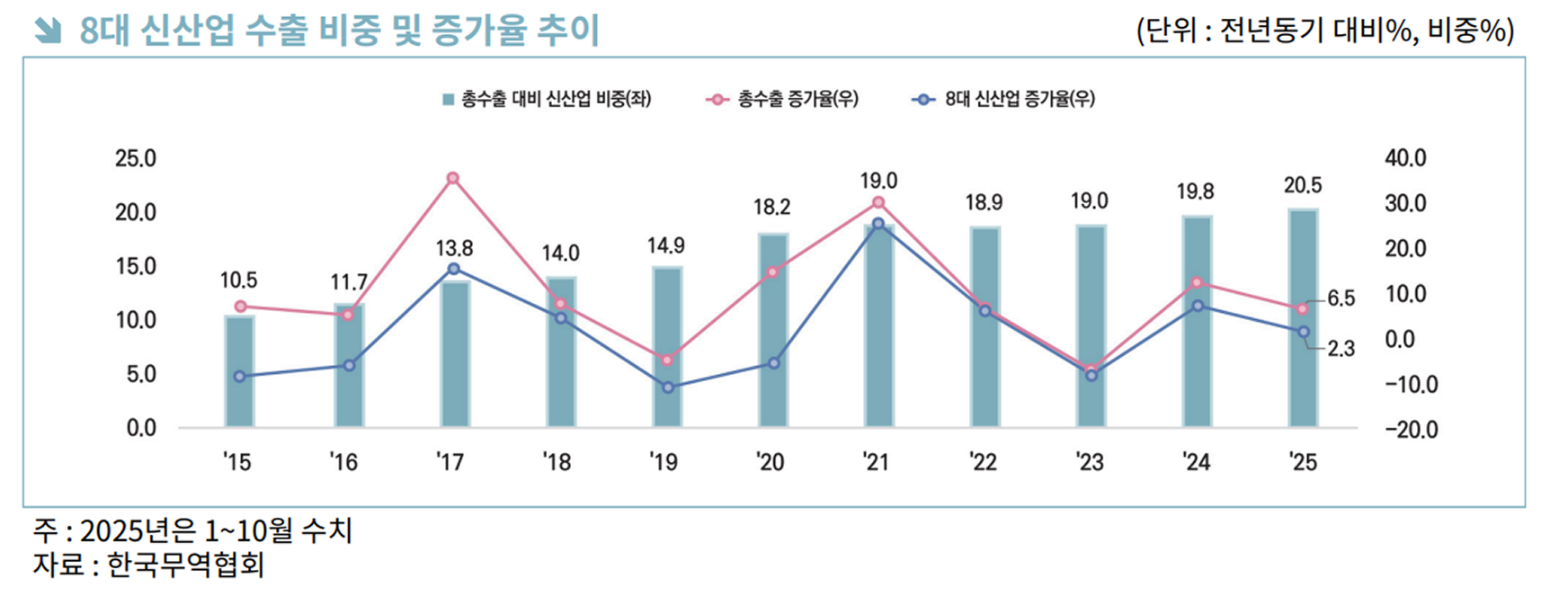

2025년 한국 수출에서 또 하나 주목할 변화는 신산업 중심의 수출 비중 확대입니다. 차세대 반도체, 바이오헬스, 차세대 디스플레이, 에너지 신산업, 전기차, 첨단 신소재, 항공우주, 로봇 등 8대 신산업의 수출 비중은 최근 10년간 약 두 배 증가하며, 전체 수출의 6.5%까지 확대되었습니다.

이러한 변화는 특정 산업의 일시적 성장이라기보다, 한국 경제와 수출 구조가 점진적으로 고부가가치 산업 중심으로 이동하고 있음을 보여주는 신호로 해석할 수 있습니다. 특히 반도체와 전기차, 첨단 소재처럼 글로벌 공급망과 직접적으로 연결된 산업의 비중이 커졌다는 점은, 향후 수출이 환율 변동이나 통상 환경 변화에 더 민감하게 반응할 가능성도 함께 시사합니다. 신산업 수출 확대는 기회인 동시에, 보다 정교한 시장·환율·공급망 관리 전략을 요구하는 국면에 진입했음을 의미합니다.

Another notable shift in Korea’s exports in 2025 was the expansion of export share driven by emerging industries. The combined export share of eight key new industries including next generation semiconductors, bio health, next generation displays, new energy industries, electric vehicles, advanced materials, aerospace, and robotics has nearly doubled over the past decade, reaching 6.5% of total exports.

This change is better understood not as temporary growth in specific sectors, but as a signal that Korea’s economy and export structure are gradually moving toward higher value added industries. In particular, the growing share of industries directly linked to global supply chains such as semiconductors, electric vehicles, and advanced materials suggests that future exports may become more sensitive to exchange rate fluctuations and changes in the trade environment. While the expansion of new industry exports presents clear opportunities, it also indicates that companies are entering a phase that requires more sophisticated market, exchange rate, and supply chain management strategies.

2025년 수출 흐름이 남긴 메시지

Key Takeaways from Export Trends in 2025

2025년 한국 무역은 단순한 회복 국면을 넘어, 양적 개선과 구조적 전환이 동시에 진행된 해로 평가할 수 있습니다. 반도체·친환경차·신산업을 중심으로 수출이 확대되는 한편, 중국과 미국 중심의 수출 구조는 점차 완화되고 EU·아세안·대만 등 제3시장 비중이 확대되었습니다. 이는 글로벌 경제 환경 변화와 환율 변동성 속에서 리스크를 분산하려는 움직임으로 볼 수 있습니다.

이러한 흐름은 2026년을 준비하는 기업들에게 분명한 시사점을 남깁니다. 수출 시장 다변화와 함께, 환율·통상 환경을 고려한 전략적 대응이 그 어느 때보다 중요해지고 있다는 점입니다.

다음 편 EP.2에서는 2026년 세계경제 및 무역환경 전망을 중심으로, 향후 글로벌 시장 흐름을 살펴볼 예정입니다.

Korea’s trade performance in 2025 can be assessed as a year in which quantitative improvement and structural transformation progressed simultaneously, going beyond a simple recovery phase. Exports expanded around semiconductors, eco friendly vehicles, and emerging industries, while reliance on China and the United States gradually eased. At the same time, the share of exports to third markets such as the EU, ASEAN, and Taiwan increased. This shift can be seen as an effort to diversify risk amid changes in the global economic environment and heightened exchange rate volatility.

These trends offer clear implications for companies preparing for 2026. Alongside export market diversification, strategic responses that take exchange rate movements and the trade environment into account are becoming more critical than ever.

In the next installment, EP.2, we will focus on the 2026 global economic and trade outlook and examine the direction of global market trends going forward.