The bearing market is showing a new growth trajectory in 2026 alongside major industrial shifts. As EVs, automation, robotics, and renewable energy industries continue to expand, bearings are gaining attention as key components that go beyond simple rotation and directly influence manufacturing competitiveness. In this article, we look at 2026 bearing market trends, regional responses, and key implications for manufacturing sites.

2026 베어링 시장 규모와 성장 전망

Global Bearing Market Size and Growth Outlook

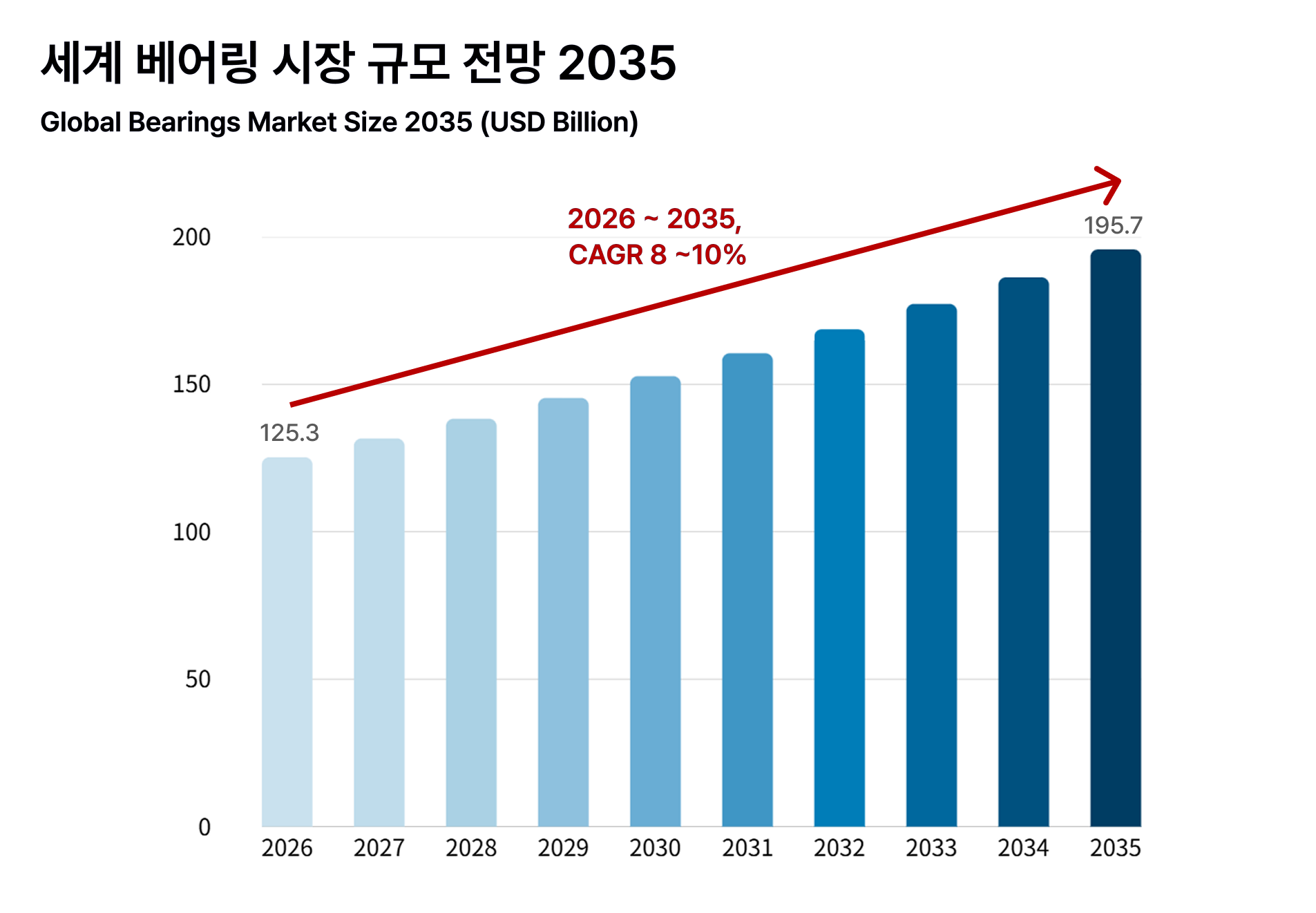

2026년 세계 베어링 시장은 안정적인 성장 흐름을 이어가고 있습니다. 시장조사 기관별 추정치에는 차이가 있지만, 2025년 약 1,200억~1,400억 달러 수준이었던 글로벌 베어링 시장은 2026년 연간 기준 약 1,500억 달러 안팎의 규모를 형성할 것으로 전망됩니다. 또한 2026년 이후 2030년대 중반까지 연평균 성장률(CAGR)은 8~10% 수준으로 예상됩니다.

이러한 성장은 단순한 수요 증가만을 의미하지 않습니다. 전기차 전환, 산업 자동화, 재생에너지 확대, 항공우주 산업 성장과 같은 구조적 변화가 베어링 시장의 방향을 바꾸고 있습니다. 회전 부품에 요구되는 성능 기준이 높아지면서, 베어링 역시 더 높은 정밀도와 내구성, 안정적인 회전 성능을 요구받고 있습니다.

베어링은 회전하는 축과 부품 사이의 마찰을 줄이고, 소음과 진동을 억제하며, 장시간 안정적인 구동을 지원하는 핵심 기계요소입니다. 따라서 베어링 시장의 성장은 단순히 부품 판매량이 늘어나는 현상이 아니라, 제조업 전반에서 고정밀·고신뢰성 부품 수요가 확대되고 있다는 신호로 볼 수 있습니다.

특히 2026년 이후 베어링 시장의 무게 중심은 범용 제품에서 고부가가치 제품으로 이동하고 있습니다. 저소음, 고속 회전, 긴 수명, 에너지 효율, 유지보수성을 갖춘 베어링이 더욱 중요해지고 있으며, 이는 정밀가공 장비와 공정 안정성에 대한 요구로도 이어지고 있습니다.

In 2026, the global bearing market continues to show a stable growth trajectory. Although estimates vary by research firm, the market, valued at approximately USD 120–140 billion in 2025, is projected to reach around USD 150 billion in 2026 on an annual basis. From 2026 through the mid-2030s, the market is expected to grow at a CAGR of approximately 8–10%.

This growth should not be understood simply as an increase in volume. Structural changes such as the EV transition, industrial automation, renewable energy expansion, and aerospace growth are reshaping the direction of the bearing market. As performance requirements for rotating components become more demanding, bearings are expected to deliver higher precision, durability, and stable rotational performance.

A bearing is a core mechanical component that reduces friction between rotating shafts and parts, helps control noise and vibration, and supports stable operation over long periods. Therefore, the growth of the bearing market reflects not only rising component demand, but also the broader manufacturing shift toward high-precision and high-reliability parts.

After 2026, the market focus is expected to move further from general-purpose products toward higher-value bearing solutions. Low noise, high-speed rotation, long service life, energy efficiency, and maintainability are becoming more important, which also increases the need for precision machining equipment and stable manufacturing processes.

베어링 산업 수요 핵심 분야: 전기차·자동화·로봇

Key Demand Drivers in the Bearing Industry: EVs, Automation, and Robotics

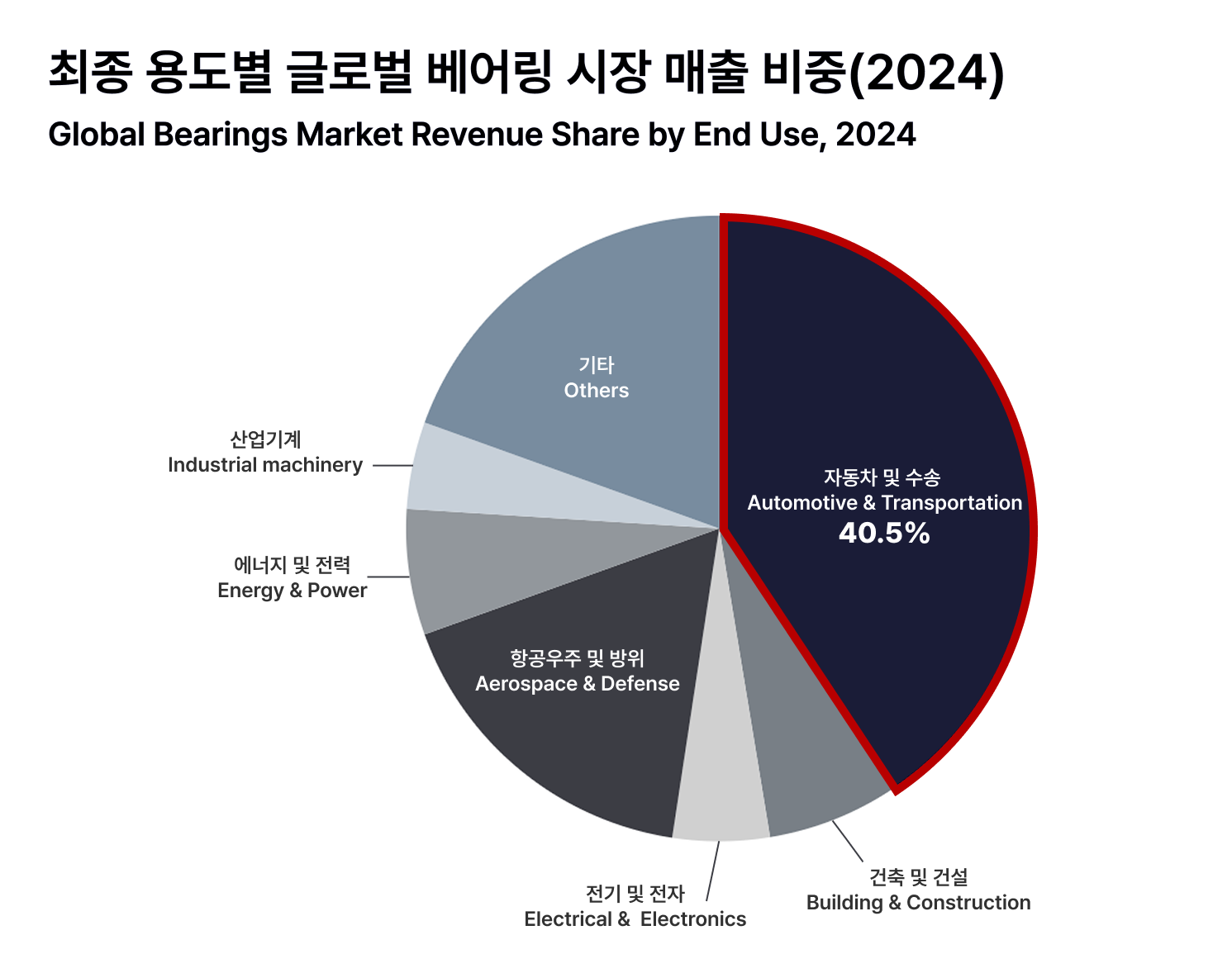

2026년 베어링 산업의 핵심 수요는 전기차, 산업 자동화, 로봇 분야를 중심으로 확대되고 있습니다. 베어링은 자동차와 수송, 항공우주와 방산, 에너지, 산업용 기계 등 다양한 산업에서 사용되지만, 그중에서도 자동차와 수송 분야는 여전히 글로벌 베어링 시장의 가장 큰 수요처로 평가됩니다.

자동차 부문에서는 볼 베어링과 롤러 베어링을 중심으로 꾸준한 수요가 이어질 것으로 예상됩니다. 일부 시장 전망에서는 자동차 부문의 베어링 시장 점유율이 2035년까지 68%를 넘어설 것으로 보고 있으며, 이는 자동차 산업이 앞으로도 베어링 수요의 중심축이 될 수 있음을 보여줍니다.

특히 전기차 전환은 자동차용 베어링의 요구 조건을 바꾸고 있습니다. 전기차 구동계는 저소음, 고속 회전, 장수명, 에너지 효율에 대한 요구가 높으며, 일부 전동화 플랫폼에서는 내연기관차 대비 20~50%가량 더 많은 베어링이 필요한 경우도 있습니다. 즉, 전기차 베어링은 사용량 증가와 고성능화가 동시에 나타나는 분야입니다.

In 2026, key bearing demand is expanding around EVs, industrial automation, and robotics. Bearings are used across many industries, including automotive and transportation, aerospace and defense, energy, and industrial machinery. Among these sectors, automotive and transportation remain the largest demand drivers in the global bearing market.

In the automotive sector, demand for ball bearings and roller bearings is expected to remain steady. Some market forecasts suggest that the automotive segment could account for more than 68% of the bearing market by 2035, showing that the automotive industry may continue to be the central axis of bearing demand.

The EV transition is also changing the performance requirements for automotive bearings. Electric drivetrains require lower noise, higher rotational speed, longer service life, and better energy efficiency. In some electrified platforms, the number of bearings required can also be 20–50% higher than in internal combustion engine vehicles. In this sense, the EV bearing market is expanding in both volume and performance requirements.

ORS Bearings ⓒ ORSKOREA 오알에스코리아

산업 로봇과 자동화 설비에서도 정밀 베어링의 중요성이 커지고 있습니다. 로봇 관절은 소형화와 경량화가 요구되는 동시에 하중을 안정적으로 지지해야 하며, 정밀 이송 장치는 부드러운 움직임과 높은 반복 정밀도를 필요로 합니다. 이에 따라 크로스 롤러 베어링, 로터리 테이블 베어링, 회전 링 베어링 등 정밀 구동용 베어링 수요도 확대될 것으로 예상됩니다.

결과적으로 2026년 베어링 수요는 단순한 물량 확대보다 저소음, 고속 회전, 장수명, 정밀도, 신뢰성을 중심으로 고도화되고 있습니다. 이러한 변화는 베어링 제조 공정에도 더 높은 가공 정밀도와 안정적인 품질 관리 역량을 요구하게 될 것입니다.

Precision bearings are also becoming more important in industrial robots and automation equipment. Robot joints require compact and lightweight designs while supporting loads reliably. Precision transfer systems require smooth motion and high repeatability. As a result, demand is expected to grow for crossed roller bearings, rotary table bearings, and slewing ring bearings used in precision motion applications.

Overall, bearing demand in 2026 is shifting beyond simple volume growth toward low noise, high-speed rotation, long service life, precision, and reliability. This trend will require higher machining accuracy and more stable quality control throughout the bearing manufacturing process.

지역별 베어링 시장 전망: 아시아·북미·유럽의 전략

Regional Bearing Market Outlook: Asia-Pacific, North America, and Europe

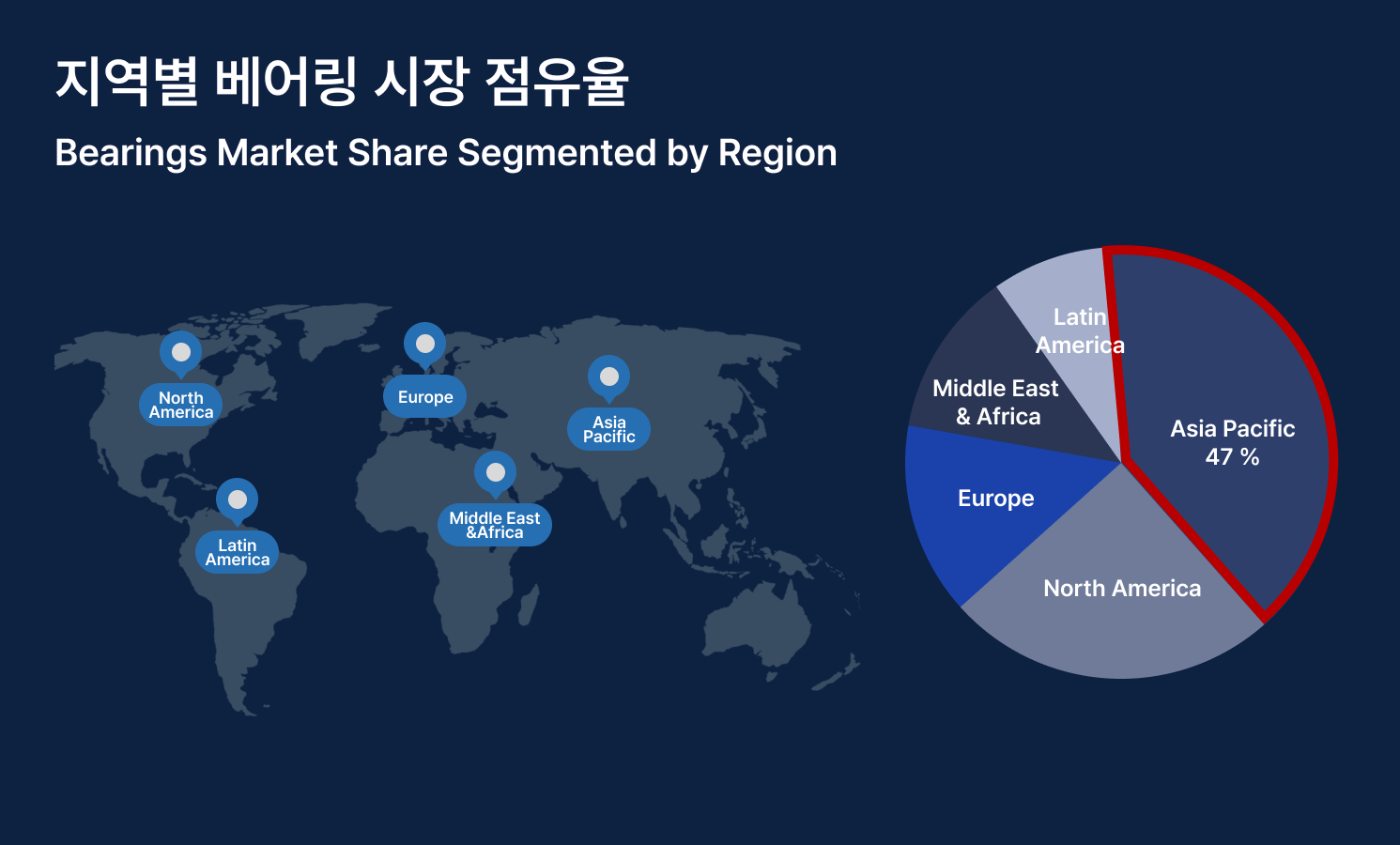

2026년 베어링 시장은 아시아·태평양, 북미, 유럽을 중심으로 지역별 성장 전략이 다르게 전개되고 있습니다. 각 지역은 산업 구조, 정책 환경, 공급망 조건이 다르기 때문에 베어링 수요 역시 동일한 방식으로 움직이지 않습니다.

가장 큰 수요 축은 아시아·태평양 지역입니다. 해당 지역은 2030년대 중반까지 글로벌 베어링 시장의 40%대 후반 수준을 차지하며 수요를 견인할 것으로 전망됩니다. 중국은 산업화와 도시화, 인프라 투자, 자동차 및 산업용 기계 수요를 기반으로 베어링 시장 확대를 이끌고 있습니다.

In 2026, the global bearing market is developing differently across Asia-Pacific, North America, and Europe. Since each region has different industrial structures, policy environments, and supply chain conditions, bearing demand is not moving in a single direction.

Asia-Pacific remains the largest demand center. The region is projected to account for the high-40% range of the global bearing market through the mid-2030s, continuing to drive overall demand. In China, industrialization, urbanization, infrastructure investment, and demand from automotive and industrial machinery sectors are supporting market expansion.

일본은 자동차, 전자 산업, 생산 자동화 분야를 중심으로 고정밀 베어링 수요가 꾸준히 형성되고 있습니다. 한국은 항공우주 연구개발과 정밀 제조 산업의 고도화 흐름 속에서 고부가가치 베어링 수요가 확대될 가능성이 있습니다.

Japan continues to generate steady demand for high-precision bearings, supported by the automotive industry, electronics manufacturing, and the wider adoption of production automation. In South Korea, demand for higher-value bearings may expand alongside aerospace R&D and the advancement of precision manufacturing industries.

북미 시장에서는 자동화, 로봇, 자동차 산업의 변화가 주요 변수로 작용하고 있습니다. 특히 관세 정책과 USMCA에 따른 북미 생산·조달 요건은 자동차 관련 베어링 공급망에 영향을 줄 수 있습니다. 이에 따라 북미 시장에서는 가격 경쟁력뿐 아니라 현지 대응력, 납기 안정성, 공급망 유연성이 중요한 경쟁 요소로 부각되고 있습니다.

유럽 시장은 재생에너지 확대와 탄소중립 정책의 영향을 받고 있습니다. 풍력, 산업 설비, 친환경 모빌리티 분야에서 베어링 수요가 이어지는 가운데, 탄소규제에 대응할 수 있는 제품 경쟁력과 현지 네트워크 확보가 중요해지고 있습니다.

결국 지역별 베어링 시장 전망은 단순히 어느 지역의 수요가 큰지를 보는 문제가 아닙니다. 각 지역의 산업 변화와 정책 조건에 맞춰 제품, 공급망, 서비스 전략을 조정할 수 있는지가 향후 글로벌 베어링 산업의 중요한 경쟁 기준이 될 것입니다.

In North America, automation, robotics, and changes in the automotive industry are key market variables. Tariff policies and USMCA-related local production and sourcing requirements may influence automotive bearing supply chains. As a result, price competitiveness, local responsiveness, lead-time stability, and supply chain flexibility are becoming more important in the North American market.

In Europe, renewable energy expansion and carbon neutrality policies are shaping bearing demand. As demand continues in wind power, industrial equipment, and sustainable mobility, companies need product competitiveness that can respond to carbon-related regulations, along with stronger local networks.

Overall, the regional bearing market outlook is not only about identifying where demand is largest. Future competitiveness in the global bearing industry will depend on how well companies can adjust their products, supply chains, and service strategies to each region’s industrial and policy conditions.

글로벌 베어링 기업의 전략: 제품·공급망·현지 대응

Strategy Shifts of Global Bearing Companies: Products, Supply Chains, and Localization

글로벌 베어링 시장의 경쟁은 이제 제품 성능만으로 결정되지 않습니다. 2026년 이후에는 지역별 산업 구조, 관세와 규제, 납기 조건, 서비스 대응력까지 함께 고려한 전략이 중요해지고 있습니다.

SKF, Schaeffler, NSK, Timken과 같은 주요 글로벌 베어링 기업들은 단순 수출 중심의 방식에서 벗어나, 지역별 수요와 정책 환경에 맞춰 제품 포트폴리오와 공급망 운영 방식을 조정하고 있습니다. 수요가 확대되는 산업에는 고부가가치 베어링과 정밀 베어링 제품군을 강화하고, 납기와 비용 부담이 큰 시장에서는 현지 조달과 서비스 네트워크를 확대하는 방식입니다.

이러한 변화는 전기차, 자동화, 로봇, 항공우주, 재생에너지처럼 품질 기준이 높은 산업에서 더욱 뚜렷하게 나타납니다. 해당 분야에서는 가격 경쟁력뿐 아니라 저소음, 고속 회전, 내구성, 신뢰성, 공급 안정성이 함께 요구됩니다.

또한 관세, 물류비, 원자재 가격, 지역별 규제는 베어링 기업의 공급망 전략에 직접적인 영향을 줍니다. 특정 국가나 생산 거점에 과도하게 의존하기보다, 시장 가까이에서 생산·조달·서비스를 운영할 수 있는 체계가 중요한 경쟁 요소로 부각되고 있습니다.

결국 글로벌 베어링 기업의 전략 변화는 하나의 방향을 보여줍니다. 앞으로의 경쟁력은 어떤 시장에 어떤 베어링을 공급할 것인지, 고객 요구에 얼마나 빠르게 대응할 것인지, 품질과 납기를 얼마나 안정적으로 유지할 것인지에 달려 있습니다.

이 흐름은 베어링 산업의 경쟁 기준이 단순한 생산량 확대에서 정밀도, 신뢰성, 공급 안정성, 제조 대응력 중심으로 이동하고 있음을 의미합니다. 따라서 2026년 이후 베어링 시장을 바라볼 때는 시장 규모나 지역별 수요뿐 아니라, 이를 실제로 구현할 수 있는 제조 기반과 공정 안정성까지 함께 살펴볼 필요가 있습니다.

Competition in the global bearing market is no longer determined by product performance alone. After 2026, companies need to consider regional industry structures, tariffs and regulations, lead-time requirements, and service responsiveness as part of their market strategy.

Major global bearing companies such as SKF, Schaeffler, NSK, and Timken are moving beyond a simple export-oriented approach. They are adjusting their product portfolios and supply chain operations according to regional demand and policy environments. For growing industries, they are strengthening higher-value and precision bearing product lines. In markets where lead time and cost pressure are high, they are expanding local sourcing and service networks.

This shift is becoming more visible in industries with demanding quality requirements, such as EVs, automation, robotics, aerospace, and renewable energy. In these sectors, customers require not only price competitiveness but also low noise, high-speed rotation, durability, reliability, and supply stability.

Tariffs, logistics costs, raw material prices, and regional regulations are also directly affecting bearing supply chain strategies. Instead of relying heavily on a single country or production base, companies are placing greater importance on production, sourcing, and service structures located closer to key markets.

Ultimately, the strategy shift of global bearing companies points in one clear direction. Future competitiveness will depend on which bearings are supplied to which markets, how quickly companies respond to customer needs, and how consistently they maintain quality and lead-time stability.

This indicates that competition in the bearing industry is shifting from simple volume expansion toward precision, reliability, supply stability, and manufacturing responsiveness. Therefore, when looking at the bearing market after 2026, it is important to consider not only market size and regional demand, but also the manufacturing foundation and process stability required to meet these changes.

2026 베어링 트렌드가 제조 현장에 주는 시사점

What 2026 Bearing Trends Mean for Manufacturing Competitiveness

2026년 이후 베어링 시장의 변화는 단순한 수요 확대가 아니라, 제조 경쟁력의 기준이 달라지고 있음을 보여줍니다. 고부가가치 베어링과 특수 베어링 수요가 확대될수록 제조 현장에는 더 높은 정밀도, 안정성, 내구성, 품질 일관성이 요구됩니다.

시장 확대는 분명한 기회이지만, 원자재 가격 변동, 공급망 리스크, 납기 관리, 환경규제와 같은 과제도 함께 커지고 있습니다. 결국 앞으로의 베어링 산업에서는 변화하는 시장 조건에 맞춰 안정적인 품질을 유지하고, 정밀한 생산 기반을 확보하는 기업이 더 큰 경쟁력을 가질 수 있습니다. 베어링 수요가 고도화될수록 이를 뒷받침하는 정밀가공 기술과 생산 설비의 역할도 더욱 중요해질 것입니다.

After 2026, the shift in the bearing market indicates more than simple demand growth. It shows that the standards for manufacturing competitiveness are changing. As demand for higher-value and specialized bearings expands, manufacturing sites will be required to secure higher precision, stability, durability, and consistent quality.

Market growth presents clear opportunities, but challenges such as raw material volatility, supply chain risks, lead-time management, and environmental regulations are also becoming more important. In the future bearing industry, companies that can maintain stable quality and build a precise production foundation will be better positioned to compete. As bearing demand becomes more advanced, the role of precision machining technology and reliable production equipment will become even more important.